1. Introduction

The rural China has undergone several institutional changes of banking in the last century [

1]. In addition, rural credit cooperative has become a dominant supplier of credit to farm production and SMEs (small and medium enterprises) in rural China since the middle of 1990s [

2]. (Cooperative is a kind of organization tackling things with cooperation or serving members based on the common interest or objective that the cooperative is intended to achieve [

3,

4]. Chinese guiding document in 1999 defines rural credit cooperative is an organization aiming at solving credit shortages of members in livelihood and agricultural production, whose members are usually rural households and offer a majority of founding capital [

5]). With continued poor performance of rural credit cooperative due to depressed prices of agricultural products and a long-lasting downturn of rural households’ income [

6], the Chinese government was forced to implement the RCC (rural credit cooperative) shareholding reform in 2003. Although led by the government, this institutional change has been transforming the institutional form of rural credit cooperative in the city and county level actually [

7]. (Chinese administrative districts consist of four levels from large to small, province, city, county, and township. Counties incorporate townships and rural areas). Depending on the operating environment and specific condition of institutions, rural credit cooperative can choose from three institutional forms: rural commercial bank based on shareholding system (a common institution of modern enterprise), rural cooperative banks based on cooperative shareholding system, or just make some improvements based on cooperative ownership before 2012. Transforming the institutional form into a shareholding system became the only choice for the rest of rural credit cooperatives and rural cooperative banks in 2012, which is regarded as the formal implementation of RCC shareholding reform [

8]. In 2019, there were 1423 headquarters and 77,258 branches of rural commercial banks [

9]. Over 80% of them are located at county areas.

Policymakers intend to realize two goals in RCC (rural credit cooperative hereafter) shareholding reform: The one is achieving financial viability through improvement of corporate governance in the shareholding system; the other is establishing small and locally owned commercial banks mainly for rural households and businesses, which has been documented as the booster of local economic development [

10,

11,

12,

13]. However, some scholars and banking staff cast doubt whether the reform is fundamental enough to achieve these goals, or formalistic, even just by changing the information in the signboards and licenses [

14]. This is because a majority of rural commercial banks look like they are keeping the same outlets location, shareholder, executive board, staff, and service after the reform [

15,

16]. The controversy leads to confusion about the effect of this reform on rural economic development. Apart from this, related empirical studies focus on the effect of RCC shareholding reform on the institution’s operating performance [

6,

17,

18,

19,

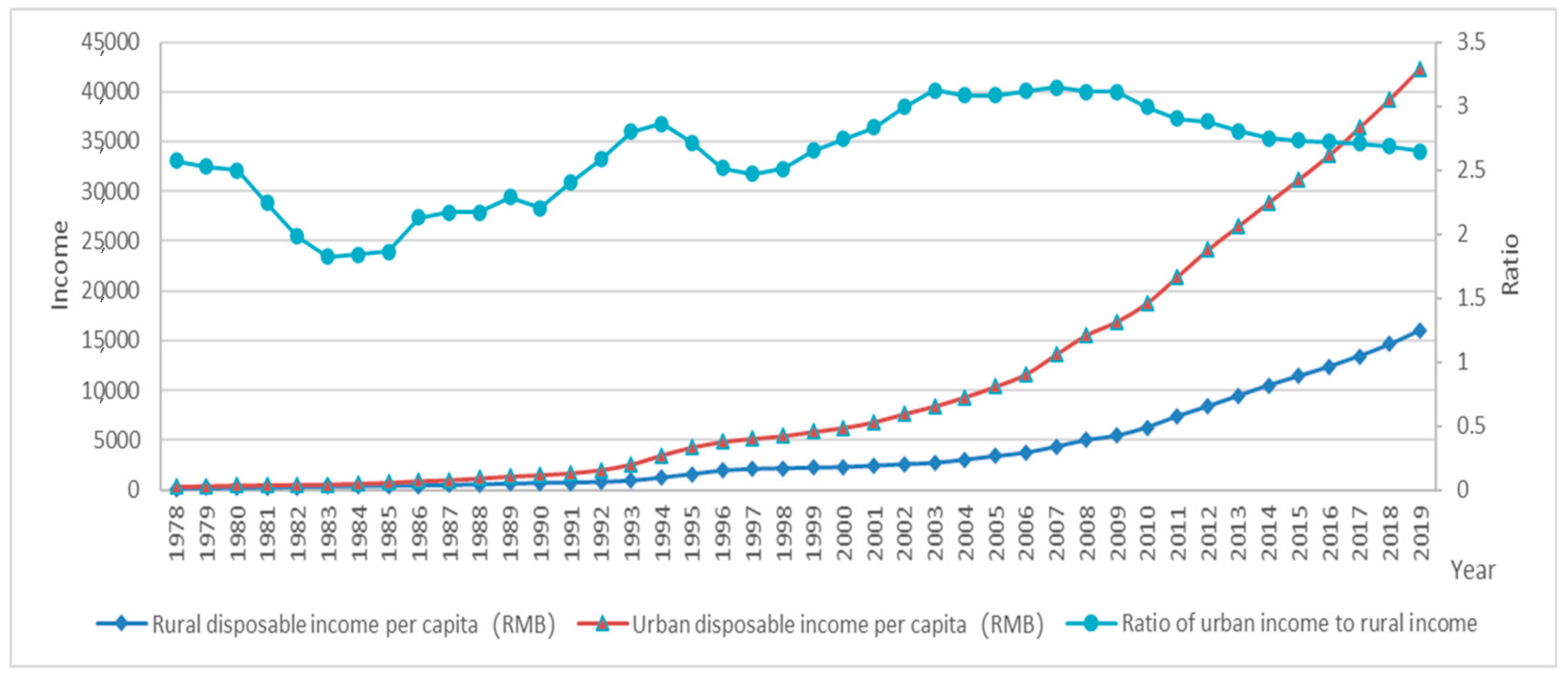

20], while its effect on rural economic development remains unanswered, which also intensifies the voice of doubt. In the context of prominent rural–urban income gap (

Figure 1), (Among several income gaps in China, urban-rural income gap is the most prominent one. It has been slightly enlarging over the past decades and the urban disposable income has been nearly 2.6 times the rural disposable income in 2019) transforming the agricultural production method into modernized mode, such as agricultural industrialization, is one of the crucial measures as it can improve agricultural productivity through specialized division of labor, scale, and intensive production and technique upgrades [

21,

22,

23,

24]. (As a modernized production, agricultural industrialization is a relationship mode for realizing a combination of production, processing, and sales, which is characterized by standardization, scale production, and specialization, and where decisions at the front-end of the supply chains are based on knowledge of the markets’ needs [

23,

24,

25]. The leading enterprise is the core part of agricultural industrialization. In January of 2021, Chinese Ministry of Agriculture and Rural Affairs released a policy to regulate the transfer of land management right in order to add further momentum to agricultural industrialization [

26]). It is urgent to establish specialized financial institutions that serve rural revitalization as China has entered the transition phase of rural revitalization after winning the battle against poverty. This confused cognizance hinders the rural commercial bank from identifying its function or responsibility clearly, and thus providing enough support to agricultural industrialization and rural revitalization firmly. According to a survey in China Family Panel Studies conducted by Peking University in 2018, only about 15% of producers engaging in scale production have access to banking loans [

27]. Therefore, we attempt to discuss the necessity of RCC shareholding reform and evaluate its performance from the perspective of rural economic development. The related results could not only strengthen the confidence of the rural commercial bank to offer stronger credit support but provide practical reference for deepening reform and promoting further development of the rural commercial bank.

Figure 1.

Chinese Rural Disposable Income, Urban Disposable Income and Urban-Rural Income Ratio from 1978 to 2019. Source: this figure is accessed from Li [

28].

Figure 1.

Chinese Rural Disposable Income, Urban Disposable Income and Urban-Rural Income Ratio from 1978 to 2019. Source: this figure is accessed from Li [

28].

Some empirical studies have provided evidences that the institutional change contributes to economic growth, despite the absence of technology upgrade sometimes [

29,

30]. There are also researches documenting the positive effect of financial institutional change on economic development [

31,

32,

33,

34]. These suggest that RCC shareholding reform may play a positive role in rural economic development. Moreover, rural commercial bank has more adequate capital and higher financial viability after relinquishing bad loans and negative equity comparing to rural credit cooperative, which strengthens their capacity to support agricultural production as well as rural economy with more capital. (The average capital adequacy ratio of rural banking institutions has increased from −8.45% in 2002 (pre-reform) to 12.97% in 2019 (in the reform). [

35]). More adequate capital of rural commercial banks enables peasants, especially smallholders, to have better access to credit. In addition, it brings more inputs, educated labor, and techniques upgrade, and thus promotes economic development in rural areas [

36,

37,

38,

39,

40,

41,

42,

43,

44]. Meanwhile, institutions after the reform have more freedom as the regulation released in the RCC shareholding reform prevents local government from interfering in the operation and management [

45]. Less intervention from the government could lower risk-taking and avoid policy lending and the resultant productivity erosion [

46,

47,

48,

49,

50]. Furthermore, Chinese Banking and Insurance Regulatory Commission (CBIRC) has tightened the regulation on the operating zone and prohibited the rural commercial bank from operating across regions, such as setting up branches at places different to the headquarters [

51,

52]. CBIRC also sets a base line on the proportion of credit extending to businesses involved with agriculture, and small and micro businesses [

53]. They both enable the funds of rural commercial bank to retain at the local areas and support rural economic development. Hence, we propose the first hypothesis that RCC shareholding reform can promote rural economic development.

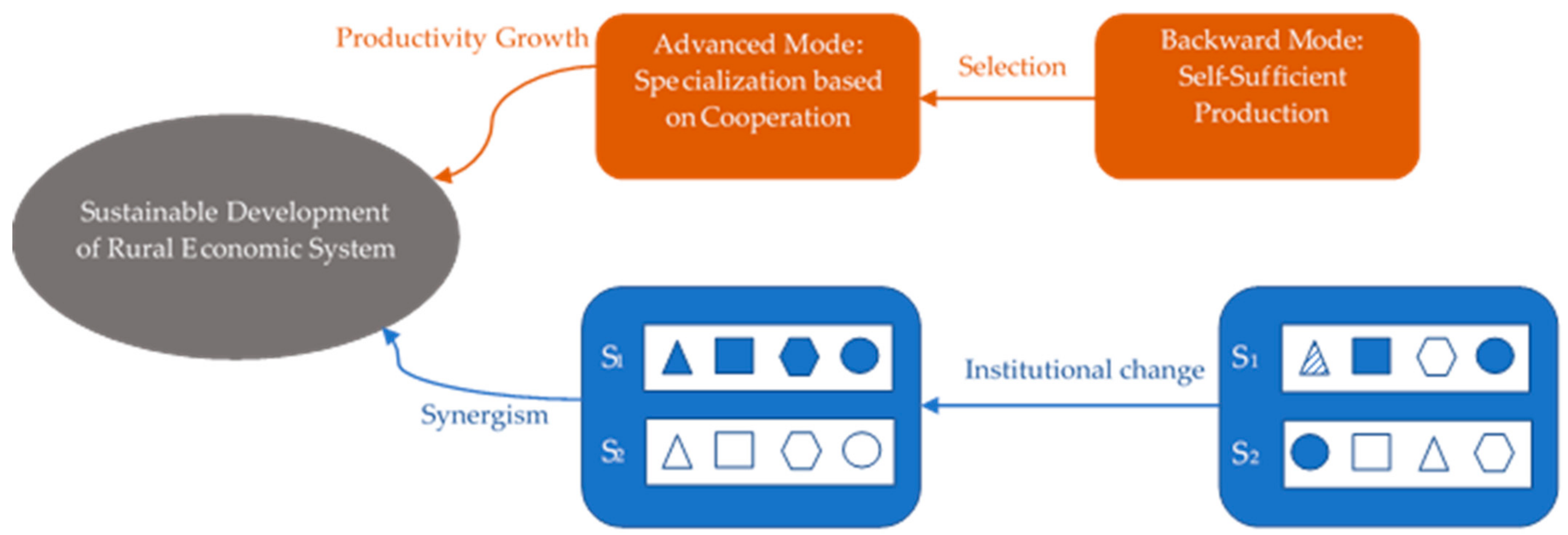

To identify the channel through which RCC shareholding reform exerts an effect, we employ the approach of system science. The investigated subjects of system science are characterized by relatively large-scale, complicated behaviors, inside interactions, and facing randomness from outside [

54,

55,

56]. Studies in social science, like economy and education, have employed this approach [

57,

58,

59,

60,

61,

62]. Following the previous study, we regard Chinese rural economy as an organic system with functions of providing agricultural products, raw materials, and jobs, which consists of an agricultural production subsystem and rural banking subsystem. (The system is defined as an organic whole with a specific function in system science [

54,

55,

63]. Elements are the basic constituents of the system and there are subsystems made up of elements in some complicated systems [

63,

64]). The evolution of a system is driven by not only the selection made by the system’s interaction with the environment, but the synergism resulting from coordinated interaction between the inside elements or subsystems [

63,

65]. Thus, in addition to the production method selected by agricultural producers and consequent productivity growth, rural economic development lies in the synergism between subsystems inside (

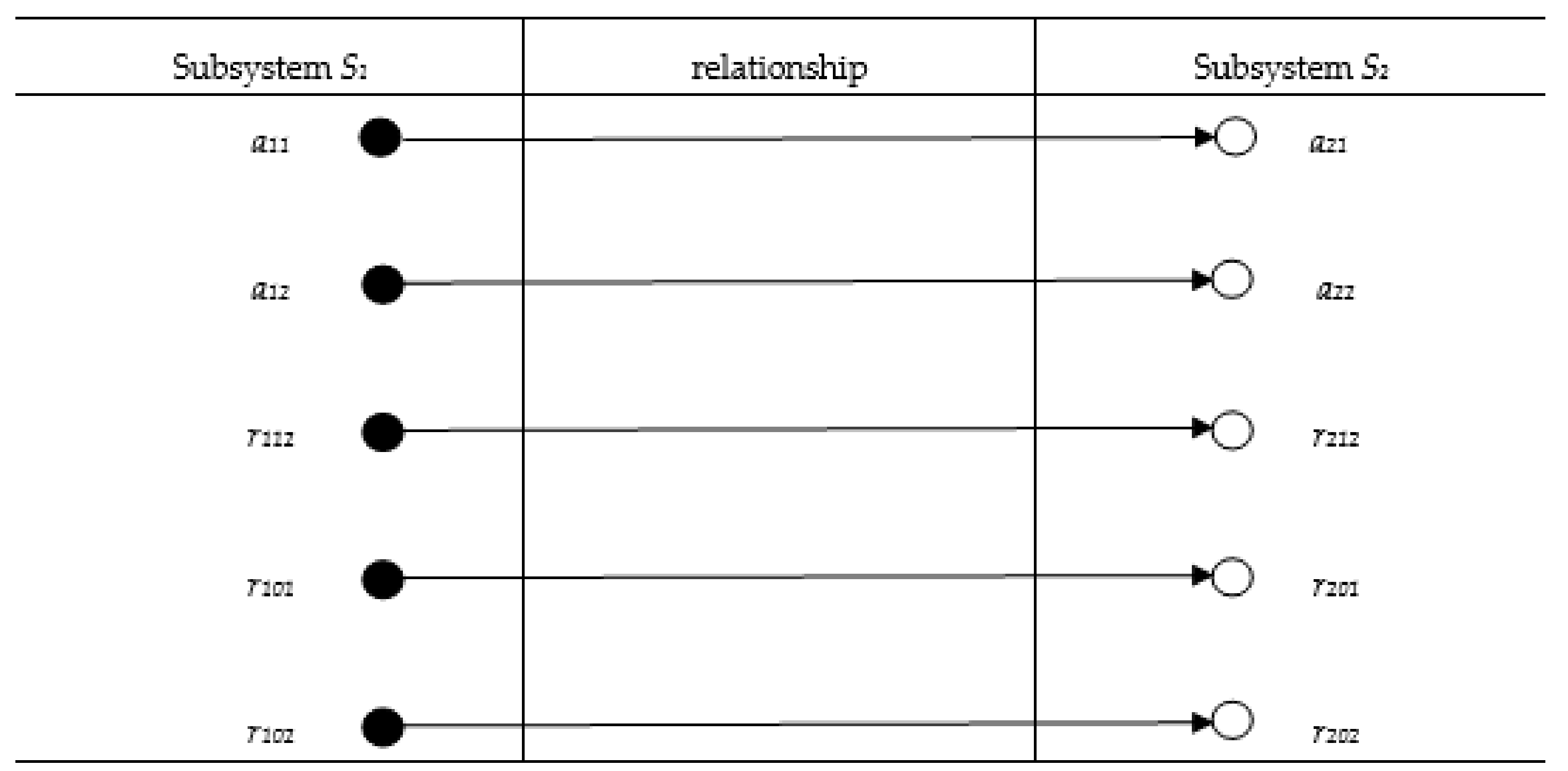

Figure 2). The rationale of isomorphic incentive compatibility underscores that subsystems can realize the coincidence of interests, coordinated interaction, and resultant synergism when there is an isomorphic relationship, namely high similarity and order in their inner structures [

63,

64,

65]. (The isomorphic relationship between systems shows that an element in a system only corresponds to a related element in another system [

64,

66]. We give a more detailed explanation in

Section 2). Institutional change usually aims at the game equilibrium among interest-related parties through shaping their interaction [

67]. Particularly, the rural commercial bank makes operating decisions such as loans granting, based on the principle of one-share-one-vote to gain maximum profits, rather than operating under one-member-one-vote for mutual aid in RCC’s period [

68,

69]. In addition, the decrement in the number of members, namely shareholders after the reform, makes ownership structure more concentrated [

69,

70]. (A survey in Shanxi Province shows that the rural credit cooperatives there have over 3000 members on average before the RCC shareholding reform [

69]. Some studies show that the shareholders’ number of rural commercial banks has decreased by over 75%, comparing to the number in the RCC period [

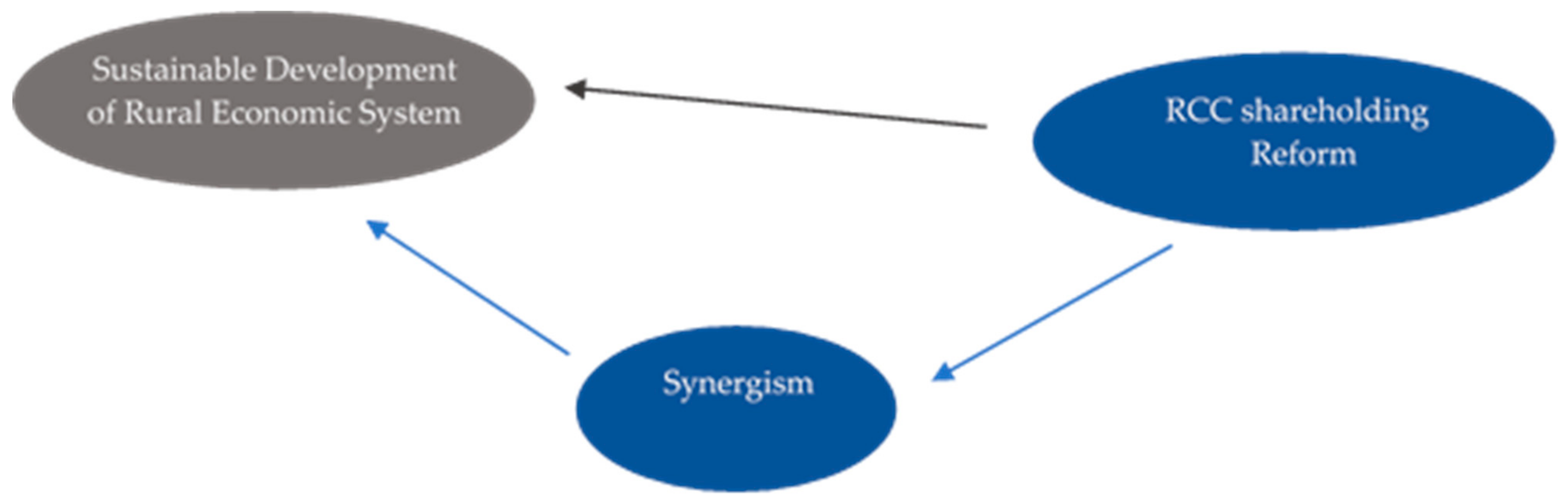

70]). Both of them make shareholders’ interests more coincident, bringing facilitation in decision-making and monitoring, and greater effectiveness of operation. Therefore, we propose the second hypothesis that promoting the synergism between rural banking institutions and agricultural producers is a plausible mechanism through which RCC shareholding reform promotes rural economic development.

To verify the two hypotheses above, we conduct this study with a sample of 30 Chinese mainland provinces, autonomous regions, and municipalities. The remainder of our study is organized as follows.

Section 2 discusses the necessity and influencing mechanism of shareholding reform. Methodology and data description are presented in

Section 3. We present empirical results and discussion in

Section 4. Conclusions are shown in the last section.

5. Conclusions and Policy Implications

Applying the rationale of system isomorphic incentive compatibility, this study evaluates the effect of Chinese RCC shareholding reform on rural economic development. We investigated whether the shareholding reform can promote agricultural growth, farmer income growth, and urban–rural gap reduction through the synergism between the agricultural production subsystem and rural banking subsystem. The theoretical analysis shows that the financial services from rural commercial banks can promote the agricultural industrialization due to their isomorphic relationship, and the similarity and order in their structures leads to the effect of incentive compatibility, which brings the synergism between two subsystems and resultant rural economic development.

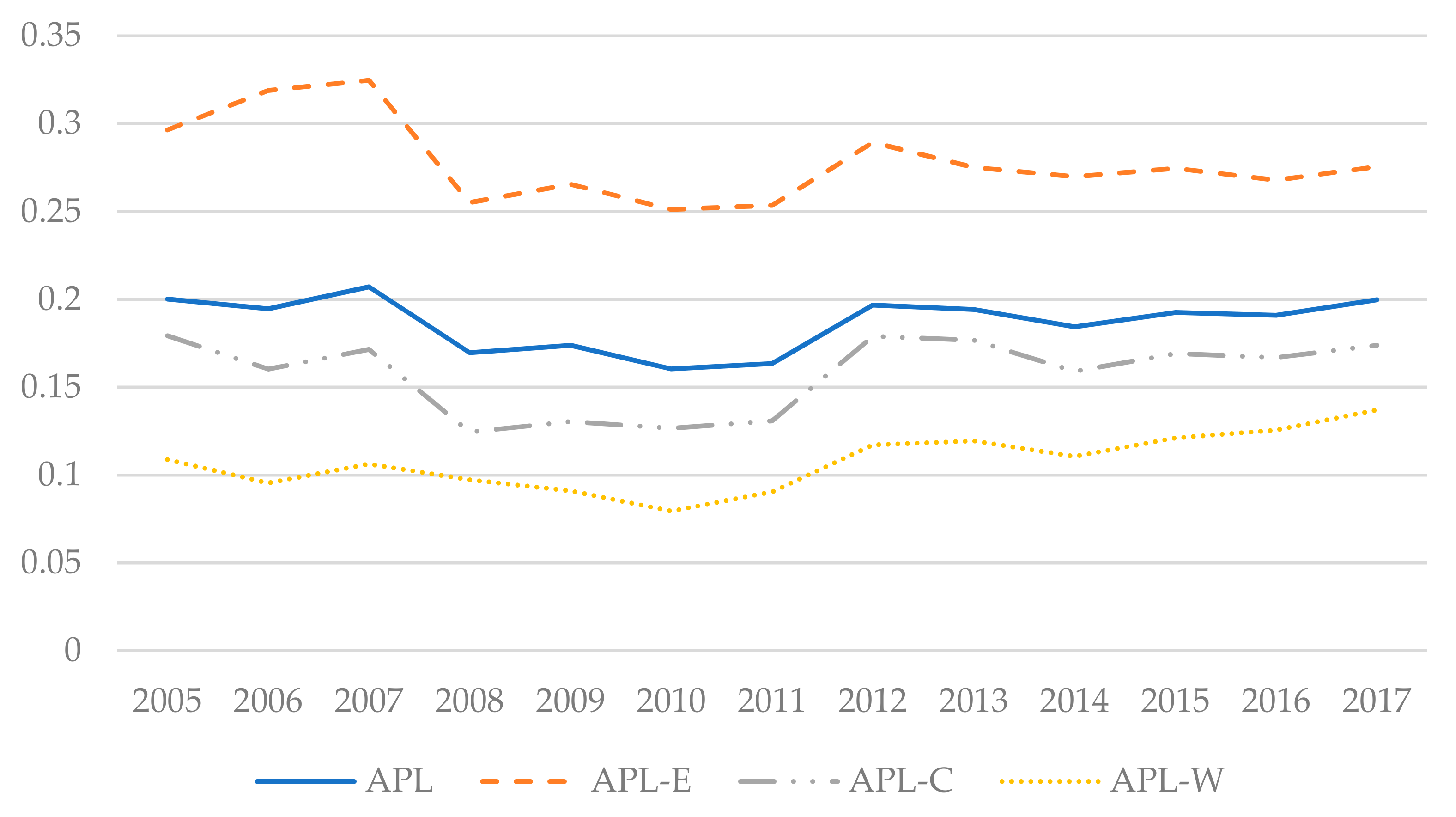

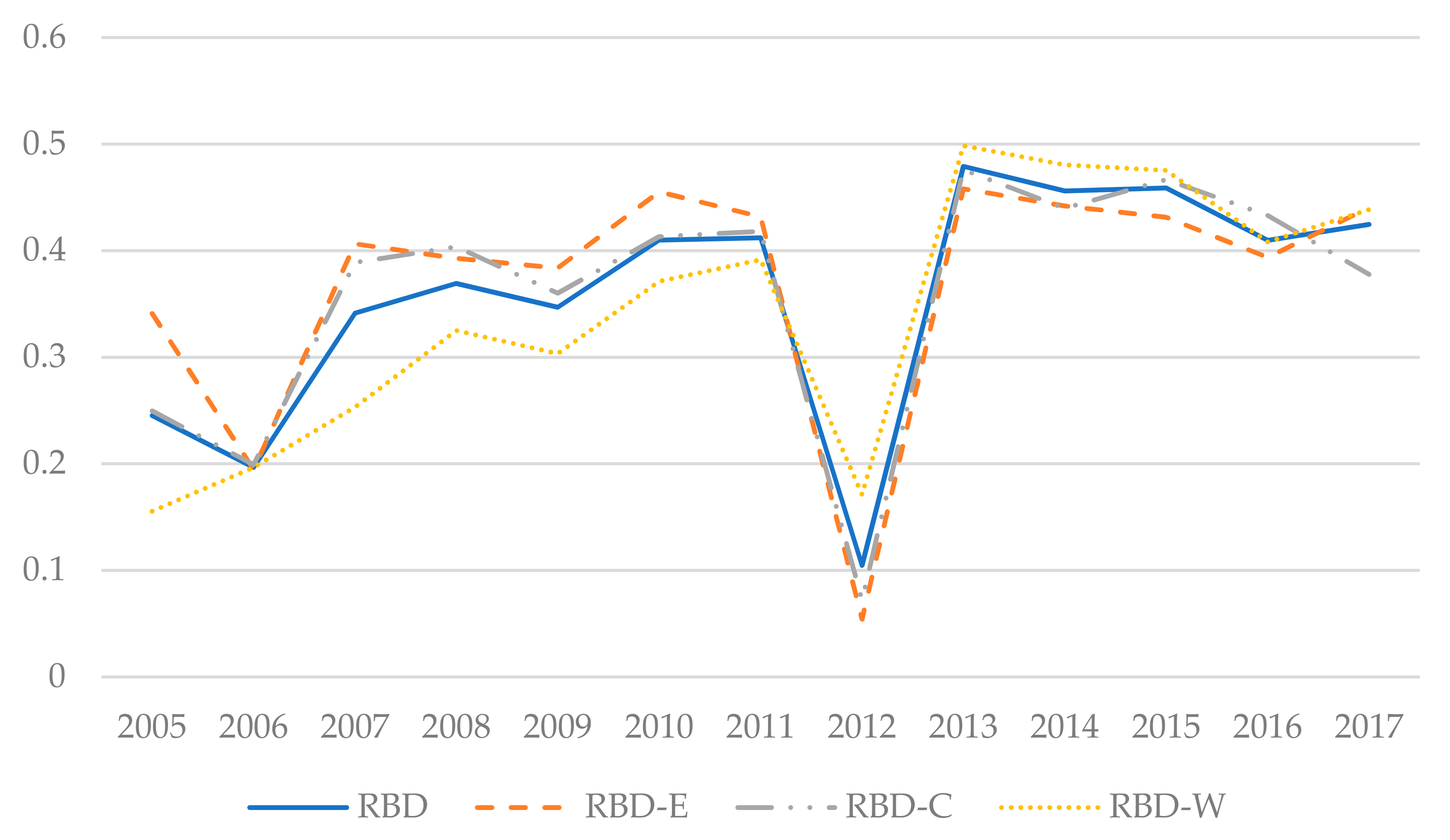

Then, we used a sample of 30 Chinese provinces, autonomous regions, and municipalities for the period 2005 to 2017 in empirical analysis. We estimate that the means of agricultural production index and rural banking development index are 0.183 and 0.371, respectively. We also calculated the coupling coordination degree between the agricultural production subsystem (agricultural production index) and rural banking subsystem (rural banking development index). The calculation result shows an obvious increase, especially after the formal implementation of shareholding reform. Comparing to provinces with lesser reform progress, the provinces with greater progress are influenced more prominently by this reform. Finally, the empirical results indicate that the synergism between two subsystems promotes agricultural growth and urban–rural income gap reduction significantly. The subsample regression shows that these effects get stronger after the formal implementation of shareholding reform in 2012. After reform, 1% increase in the coupling coordination degree could improve the agricultural growth by 0.7758% and reduce the urban-rural income gap by 0.3850% significantly.

Comparing to other studies involved with the rural reform, our study explains the mechanism from the perspective of system science and verifies that RCC shareholding reform plays a positive role in rural economic development through promoting the synergism between the agricultural production subsystem and rural banking subsystem. It makes three-fold contributions to the literature. First, a large body of literature concentrates on the performance of rural reforms on land, taxation, and household immigration from the perspective of agricultural development or agricultural productivity. We examine the effect of reform in rural banking institutions. Second, although existing literature documents the reform-growth nexus in agriculture, farmer income and so on [

100,

101,

102,

103,

104,

105,

106,

107], they have not identified whether the coordinated interaction and consequent synergism between subsystems inside is the plausible influencing channel. This study estimates the synergism between two subsystems proxied by coupling coordination degree and investigates the effect of the synergism on agricultural growth, farmer income growth, and urban–rural income gap reduction. Finally, we discuss the theoretical mechanism with the rationale of isomorphic incentive compatibility in system science. Specifically, the sustainable development of the rural economic system lies in synergism between its subsystems, which results from their highly similar and ordered structure, balanced interaction, and incentive compatibility. It sheds a light on the study associated with sustainability in rural economy from the perspective of the system science.

This study can provide practical references to both policy makers related with the rural economic development or the shareholding reform and help rural commercial bank function better. First, since RCC shareholding reform is necessary in the process of agricultural industrialization, local government could promote rural economic development through pushing forward the RCC shareholding reform. Second, attention should be paid to not only the development of a single subsystem, but also the synergism between subsystems of the rural economy system. For example, it is not enough to take the improvement of rural banking institutions into consideration. Rather, how to stimulate the synergism between rural banking subsystem and agricultural production subsystem should also become an emphasis in the work of policymakers and rural banking staff. Meanwhile, the leading enterprises in agricultural industrialization and enterprises with government background can become the shareholders of rural commercial banks and participate in the corporate governance in line with requirements. The appropriate participation of government-related enterprises can avoid rural commercial banks serving as leading enterprises solely. Besides, peasants should realize that entering the modernized mode of production makes them more accessible to credit and that they need to cooperate with rural banking institutions rather than regard themselves as the financially excluded. In addition, they also can choose to become the representative of small holders and participate in corporate governance of rural commercial banks. Furthermore, considering the geographic differences in the agricultural production and rural banking development, the focus of their development should vary among regions accordingly.

However, there are some limitations that might be addressed by analysis in the future. A majority of rural commercial banks’ headquarters are located in the county areas, which indicates that it is more appropriate to examine the effect of reform at the county level. However, data on rural banking development is only available at the provincial level, which is unable to measure the level of rural banking subsystem at county level. Due to the data unavailability, we cannot employ a specialized policy evaluation approach to verify whether synergism between two subsystems is the influencing mechanism of reform, such as difference-in-difference (DID), either.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}